2026 Debt Consolidation Guide: Reduce Payments by 18% & Save

The 2026 Guide to Debt Consolidation: Reducing Your Monthly Payments by 18%

Are you feeling overwhelmed by multiple debts, high-interest rates, and confusing payment schedules? You’re not alone. In 2026, many individuals and families are grappling with the complexities of managing their finances. The good news is that there’s a powerful strategy that can help you regain control: debt consolidation 2026. This comprehensive guide will walk you through everything you need to know about consolidating your debt, with a focus on how you can potentially reduce your monthly payments by an impressive 18%.

As the financial landscape evolves, so do the tools and strategies available for debt management. This article is your up-to-date resource, tailored for the current economic climate. We’ll delve into the benefits, types, and practical steps for effective debt consolidation 2026, ensuring you have the knowledge to make informed decisions and pave your way to financial stability.

Understanding Debt Consolidation: A 2026 Perspective

At its core, debt consolidation 2026 is the process of combining multiple debts into a single, more manageable payment. Imagine having several credit card bills, a personal loan, and perhaps some medical debt, each with different interest rates, due dates, and terms. It can be a juggling act that leads to stress and missed payments. Consolidation simplifies this by rolling all these separate obligations into one new loan or payment plan. This often results in a lower overall interest rate and a more extended repayment period, which directly translates to reduced monthly payments.

Why is Debt Consolidation More Relevant in 2026?

The year 2026 brings its own set of economic nuances. Interest rates have seen fluctuations, consumer debt levels have shifted, and new financial products have emerged. Understanding these factors is crucial for successful debt consolidation 2026. With advanced financial technology and a more competitive lending market, consumers have more options than ever before. However, navigating these options requires a clear understanding of what’s available and what best suits your individual financial situation.

The primary appeal of debt consolidation 2026 is its ability to streamline your financial obligations. Instead of remembering multiple due dates and making several payments each month, you’ll have just one. This not only reduces the chances of missing a payment but also frees up mental bandwidth. Furthermore, if you secure a lower interest rate, more of your payment will go towards paying down the principal balance, accelerating your journey out of debt.

The Potential for 18% Reduction in Monthly Payments

The promise of reducing your monthly payments by 18% through debt consolidation 2026 is a significant motivator for many. While this figure is an average and individual results may vary, it highlights the substantial savings potential. How is such a reduction achieved?

Lower Interest Rates

One of the main ways debt consolidation 2026 helps reduce payments is by securing a lower interest rate. High-interest debts, such as credit card balances, can accumulate rapidly, making it difficult to pay down the principal. By consolidating these debts into a new loan with a significantly lower interest rate, more of your monthly payment goes towards the actual debt, rather than just covering interest charges. In 2026, lenders are offering competitive rates for qualified borrowers, making this a prime opportunity to capitalize on lower rates.

Extended Repayment Terms

Another factor contributing to reduced monthly payments is the ability to extend the repayment term. While a longer term might mean paying more interest over the life of the loan, it significantly lowers your immediate monthly burden. For individuals struggling to meet current payment obligations, this breathing room can be invaluable. It allows you to free up cash flow for other essential expenses or to build an emergency fund, providing a more stable financial foundation.

Eliminating Multiple Fees

When you have multiple debts, you’re often subjected to various fees – late payment fees, annual fees, and even over-limit fees. Debt consolidation 2026 can help eliminate these recurring charges by combining everything into one payment with potentially fewer associated fees. This seemingly small saving can add up over time, further contributing to the overall reduction in your financial outflow.

Types of Debt Consolidation Methods in 2026

The world of debt consolidation 2026 offers several avenues, each with its own advantages and disadvantages. Understanding these options is key to choosing the right path for your financial situation.

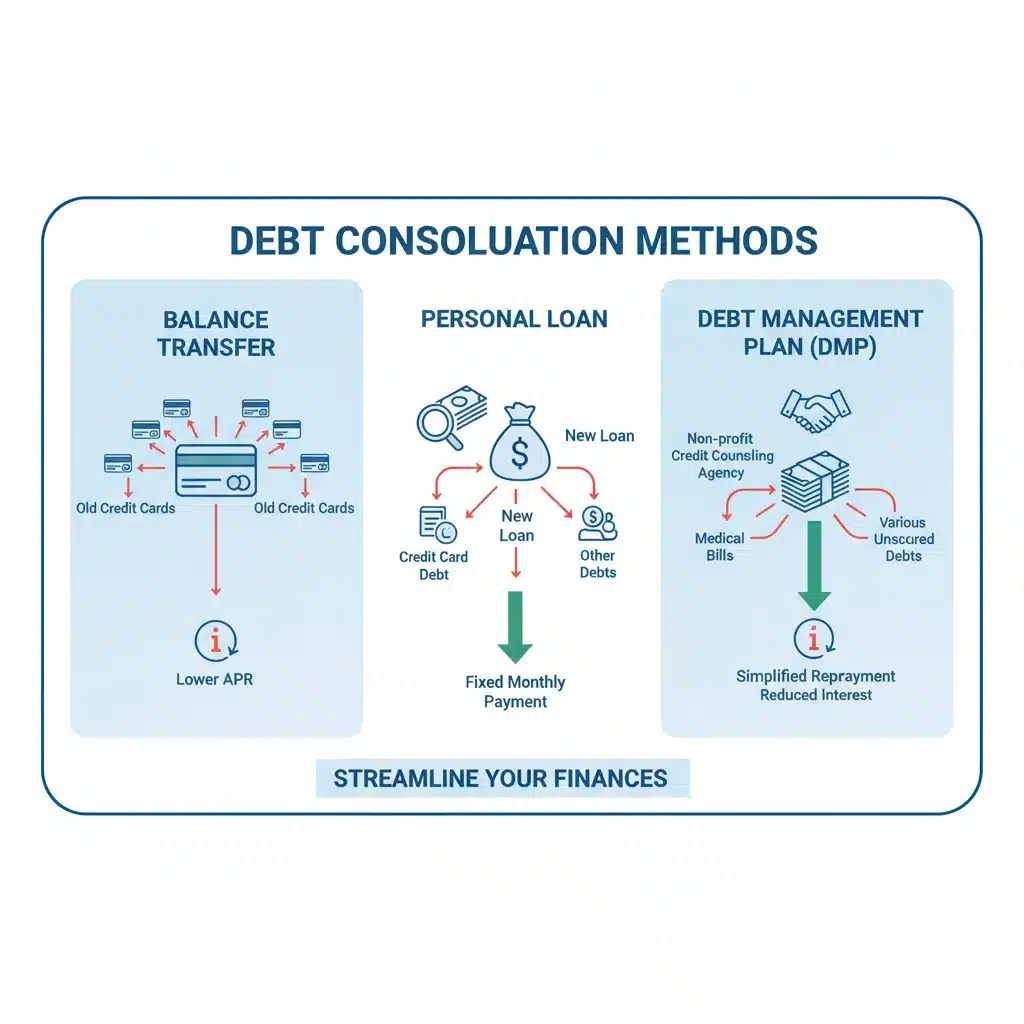

1. Personal Loans for Debt Consolidation

A personal loan is one of the most common and straightforward ways to consolidate debt. You take out a new, unsecured loan for the total amount of your existing debts. Once approved, the funds are used to pay off all your other creditors, leaving you with a single monthly payment to the personal loan lender. In 2026, personal loan rates are highly competitive, especially for borrowers with good credit scores. This method is excellent for those looking for a fixed interest rate and a predictable repayment schedule.

Pros:

- Fixed interest rates and predictable monthly payments.

- Clear end date for debt repayment.

- Often lower interest rates than credit cards.

Cons:

- Requires a decent credit score for the best rates.

- Can be tempting to incur new debt if old credit lines are not closed.

2. Balance Transfer Credit Cards

Another popular strategy for debt consolidation 2026 involves using a balance transfer credit card. These cards often offer an introductory 0% APR period (typically 12-21 months) on transferred balances. If you can pay off your debt within this promotional period, you could save a significant amount on interest. However, it’s crucial to be mindful of balance transfer fees, which usually range from 3% to 5% of the transferred amount.

Pros:

- 0% interest for an introductory period can lead to substantial savings.

- Ideal for those who can pay off debt quickly.

Cons:

- Requires excellent credit to qualify for the best offers.

- Balance transfer fees apply.

- High interest rates kick in after the promotional period if the balance isn’t paid off.

3. Home Equity Loans or Lines of Credit (HELOCs)

For homeowners, utilizing home equity through a home equity loan or HELOC can be an attractive option for debt consolidation 2026. These are secured loans, meaning your home serves as collateral. Because of this, they typically offer lower interest rates than unsecured personal loans or credit cards. A home equity loan provides a lump sum, while a HELOC offers a revolving line of credit you can draw from as needed.

Pros:

- Very low interest rates due to being a secured loan.

- Interest may be tax-deductible (consult a tax professional).

- Can consolidate a large amount of debt.

Cons:

- Your home is at risk if you default on payments.

- Closing costs and fees can apply.

- Can take longer to process than other options.

4. Debt Management Plans (DMPs)

Administered by non-profit credit counseling agencies, a Debt Management Plan (DMP) is a structured approach to debt consolidation 2026. The agency negotiates with your creditors on your behalf to reduce interest rates, waive fees, and set up a single, affordable monthly payment. You make one payment to the agency, and they distribute the funds to your creditors. DMPs don’t involve taking out a new loan, making them suitable for those who may not qualify for other consolidation methods due to credit issues.

Pros:

- Lower interest rates and waived fees can be negotiated.

- No new loan required.

- Provides professional guidance and support.

- Can improve credit score over time with consistent payments.

Cons:

- May require closing existing credit card accounts.

- Not all creditors participate.

- Monthly fees for the service may apply.

5. Reverse Mortgages (for Seniors)

For eligible seniors (typically 62 and older in the US) with significant home equity, a reverse mortgage can be a consideration for debt consolidation 2026. This allows homeowners to convert a portion of their home equity into cash without having to sell the home or make monthly mortgage payments. The loan balance becomes due when the last borrower leaves the home permanently. While it can free up cash, it’s a complex financial product with significant implications and requires careful consideration and professional advice.

Pros:

- Eliminates monthly mortgage payments.

- Provides tax-free cash for debt repayment.

Cons:

- Can deplete home equity over time.

- Fees and closing costs can be high.

- Heirs inherit a larger loan balance.

Steps to Successfully Consolidate Your Debt in 2026

Embarking on the journey of debt consolidation 2026 requires a systematic approach. Here’s a step-by-step guide to help you navigate the process effectively:

Step 1: Assess Your Current Debt Situation

Before you can consolidate, you need to know exactly what you’re dealing with. List all your debts, including credit cards, personal loans, medical bills, and any other unsecured debts. For each debt, note down:

- The outstanding balance

- The interest rate

- The minimum monthly payment

- The due date

This comprehensive overview will give you a clear picture of your financial obligations and help you calculate your total debt and current monthly outflow. This initial assessment is vital for determining how much you can potentially save through debt consolidation 2026.

Step 2: Check Your Credit Score

Your credit score plays a significant role in determining the interest rates and terms you’ll qualify for. A higher credit score generally leads to better offers. Obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) and review them for any inaccuracies. Addressing errors can potentially boost your score before applying for new credit for debt consolidation 2026.

Step 3: Research and Compare Consolidation Options

Based on your debt assessment and credit score, explore the different consolidation methods discussed above. Consider which option aligns best with your financial goals and risk tolerance. Don’t just look at the lowest interest rate; also factor in fees, repayment terms, and the reputation of the lender or agency. For instance, if you have excellent credit, a personal loan or balance transfer card might be ideal. If your credit isn’t perfect, a DMP could be a better fit for your debt consolidation 2026 strategy.

Step 4: Apply for Your Chosen Consolidation Method

Once you’ve selected a method, proceed with the application. Be prepared to provide financial documentation, such as proof of income, bank statements, and details of your existing debts. Be honest and thorough in your application to avoid delays.

Step 5: Pay Off Your Old Debts

If you’re approved for a personal loan or balance transfer card, use the funds to immediately pay off your high-interest debts. It’s crucial not to spend this money on anything else. Confirm with your previous creditors that the balances have been paid in full and that your accounts are closed or marked as paid. This step is critical to ensure proper debt consolidation 2026.

Step 6: Develop a New Budget and Stick to It

With your debts consolidated into a single, more manageable payment, now is the time to create a new budget. Factor in your new monthly payment and ensure you have enough money left over for essential expenses and savings. The goal is not just to consolidate debt but to prevent accumulating new debt. This is perhaps the most important step for long-term financial success with debt consolidation 2026.

Step 7: Avoid Incurring New Debt

This cannot be stressed enough. For debt consolidation 2026 to be truly effective, you must break the cycle of debt. Resist the temptation to use your newly freed-up credit lines. Consider closing old credit card accounts if you don’t trust yourself not to use them. Focus on living within your means and building a financial safety net.

The Evolving Landscape of Debt Management in 2026

The financial world is dynamic, and 2026 brings new considerations for those looking to consolidate debt. Technological advancements, regulatory changes, and economic shifts all play a role in shaping the options available.

FinTech Innovations

Financial technology (FinTech) continues to revolutionize lending. In 2026, we see more sophisticated algorithms for credit assessment, leading to faster approvals and potentially more personalized loan offers. Online lenders are often more agile than traditional banks, offering competitive rates and streamlined application processes for debt consolidation 2026.

Regulatory Environment

Governments and regulatory bodies are constantly reviewing consumer protection laws. Stay informed about any new regulations that might impact lending practices, interest rate caps, or credit counseling services. These changes could either open up new opportunities or introduce new safeguards for consumers undertaking debt consolidation 2026.

Economic Outlook

The broader economic climate in 2026 will influence interest rates and lender willingness. If interest rates are generally low, it’s an opportune time to lock in a favorable rate for a consolidation loan. Conversely, if rates are rising, acting sooner rather than later might be beneficial. Keeping an eye on economic forecasts can help you time your debt consolidation 2026 efforts effectively.

Potential Pitfalls and How to Avoid Them

While debt consolidation 2026 offers significant benefits, it’s not without its risks. Being aware of these potential pitfalls can help you navigate the process more safely.

1. Accumulating New Debt

The most common mistake people make after consolidating debt is to run up new balances on their old credit cards. This leaves them in a worse position than before, with a new consolidation loan and renewed high-interest debt. Avoid this by closing accounts, cutting up cards, and committing to a strict budget.

2. High Fees and Hidden Costs

Some consolidation options, particularly balance transfers or certain debt relief programs, come with upfront fees. Always read the fine print and ensure you understand all costs involved. A seemingly low interest rate can be negated by excessive fees. Always ask for a clear breakdown of all charges before committing to any debt consolidation 2026 solution.

3. Scams and Predatory Lenders

Unfortunately, the debt relief industry can attract unscrupulous actors. Be wary of companies that promise unrealistic results, demand upfront payment before doing any work, or pressure you into making quick decisions. Always verify the credentials of any company or agency you consider working with for debt consolidation 2026.

4. Impact on Credit Score

While debt consolidation 2026 can improve your credit score in the long run by demonstrating responsible payment behavior, there can be a temporary dip. Applying for new credit involves a hard inquiry, and closing old accounts can slightly reduce your available credit. Understand these short-term effects and plan accordingly.

Maximizing Your Savings with Debt Consolidation in 2026

Beyond simply reducing your monthly payments, there are strategies you can employ to maximize the long-term savings and benefits of debt consolidation 2026.

Aggressive Repayment

If your financial situation improves, consider making extra payments on your consolidated loan. Even small additional amounts can significantly reduce the total interest paid and shorten the repayment period. This accelerated repayment strategy is a powerful way to leverage your debt consolidation 2026 efforts.

Automate Payments

Set up automatic payments for your consolidated loan. This ensures you never miss a payment, which protects your credit score and helps you avoid late fees. Consistency is key to successful debt repayment.

Build an Emergency Fund

Once your monthly payments are reduced, redirect some of those freed-up funds into an emergency savings account. A robust emergency fund can prevent you from falling back into debt when unexpected expenses arise, solidifying the positive impact of your debt consolidation 2026.

Continue Monitoring Your Credit

Regularly check your credit report and score. This helps you track your progress, identify any potential issues, and ensure that your responsible debt management is being accurately reflected. A good credit score will open up more financial opportunities in the future.

Case Studies: Real-World Impact of Debt Consolidation 2026

To illustrate the power of debt consolidation 2026, let’s look at hypothetical scenarios:

Case Study 1: Sarah’s Credit Card Debt

Sarah had three credit cards with a combined balance of $15,000, average interest rates of 22%, and minimum monthly payments totaling $550. She secured a personal loan for $15,000 at a 10% interest rate over 48 months. Her new monthly payment became approximately $380, representing a 31% reduction in monthly payments. This allowed her to build an emergency fund and avoid falling behind on other bills.

Case Study 2: Mark’s Diverse Debts

Mark had a personal loan, some medical bills, and a couple of store credit cards, totaling $25,000. His average interest rate was 18%, and minimum payments were $700. He opted for a Debt Management Plan through a non-profit agency. The agency negotiated his interest rates down to an average of 9% and extended his repayment period. His new single payment was $575, a 17.8% reduction, making his financial life much more manageable.

These examples highlight how debt consolidation 2026 can be a game-changer, providing not just financial relief but also peace of mind.

The Future of Debt Management: Beyond 2026

As we look beyond 2026, the landscape of debt management will continue to evolve. Artificial intelligence and machine learning are poised to offer even more personalized financial advice and automated debt repayment strategies. Blockchain technology could also play a role in creating more transparent and secure lending platforms. Staying informed and adaptable will be key to managing your finances effectively in the years to come.

Embracing proactive financial planning, including strategic use of tools like debt consolidation 2026, will empower you to navigate future economic shifts with confidence. The goal is not just to get out of debt, but to build lasting financial resilience.

Conclusion: Your Path to Financial Freedom Starts Now

Debt consolidation 2026 offers a powerful pathway to simplify your finances, reduce your monthly payments, and accelerate your journey towards being debt-free. By understanding the various methods, carefully assessing your situation, and making informed choices, you can achieve significant savings, potentially reducing your monthly outflows by 18% or more.

Remember that successful debt consolidation is not a one-time fix but rather a strategic move within a broader financial plan. Commit to responsible spending, maintain a budget, and leverage the breathing room created by lower payments to build a stronger financial future. The time to take control of your debt is now, and with the insights provided in this 2026 guide, you are well-equipped to make it happen.

Don’t let debt dictate your life. Explore your debt consolidation 2026 options today and take the definitive step towards financial peace and freedom.