2026 Social Security Benefits: New Calculations & 1.5% Impact on Retirement

In the ever-evolving landscape of retirement planning, staying informed about future Social Security adjustments is paramount. As we look ahead to 2026 Social Security Benefits, there’s significant discussion surrounding new calculations and their potential impact on your retirement income. This comprehensive guide will delve into what these changes entail, particularly the projected 1.5% adjustment, and how they could shape your financial future.

Social Security remains a cornerstone of retirement for millions of Americans. Understanding how your benefits are calculated, and what factors influence those calculations, is crucial for effective financial planning. The year 2026 is poised to bring specific adjustments that could alter the trajectory of your retirement income, making it essential to grasp the nuances of these upcoming changes.

The Social Security Administration (SSA) continually evaluates economic conditions, inflation rates, and demographic shifts to determine future benefit levels. These evaluations often lead to adjustments in various components of the benefit formula, which can have a ripple effect on individual payouts. For those nearing retirement or already receiving benefits, these updates are not merely statistical figures; they represent real-world implications for their monthly income and overall financial security.

This article aims to demystify the complexities surrounding 2026 Social Security Benefits. We will explore the mechanisms behind benefit calculations, discuss the factors leading to the projected 1.5% impact, and provide actionable insights for navigating these changes. Our goal is to equip you with the knowledge needed to make informed decisions and optimize your retirement strategy in light of these anticipated modifications.

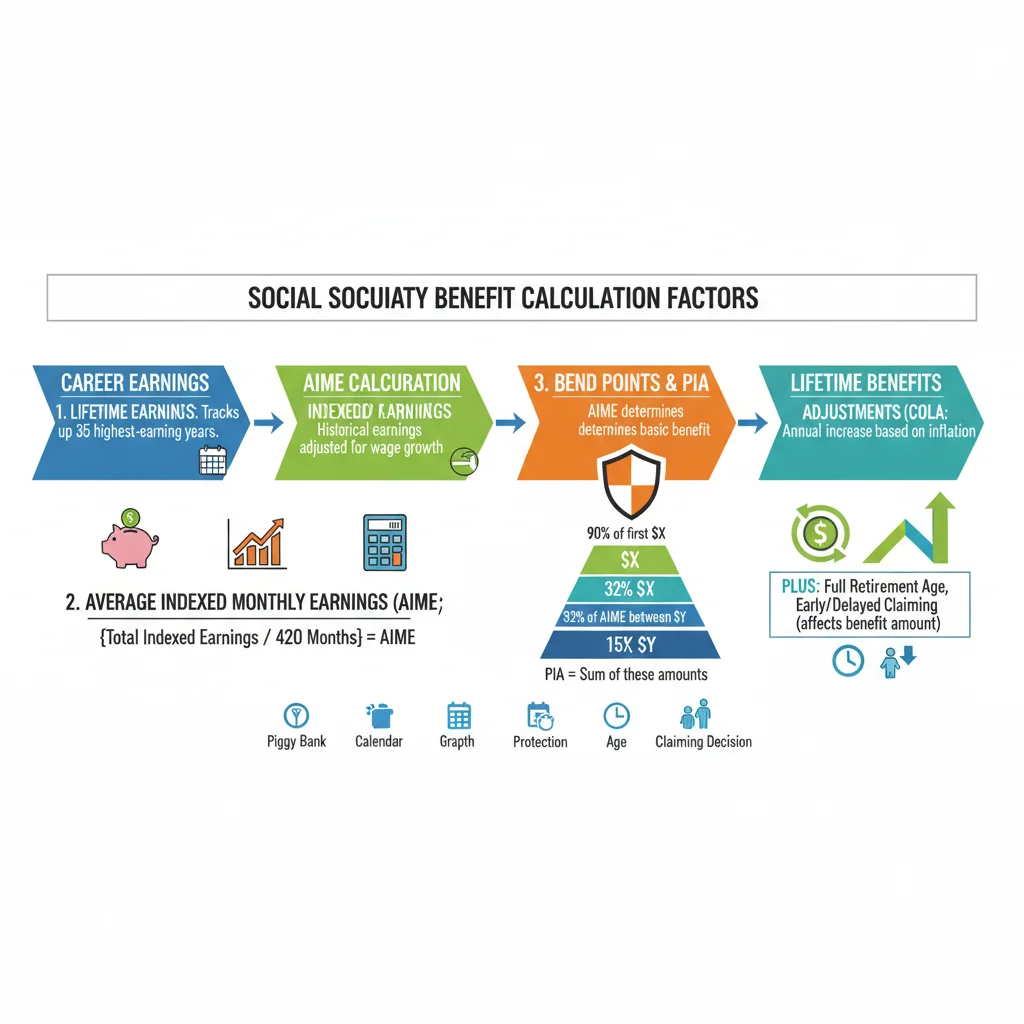

Understanding the Basics of Social Security Benefits

Before we dive into the specifics of 2026 Social Security Benefits, it’s helpful to revisit the fundamental principles governing how Social Security benefits are calculated. Your retirement benefits are primarily based on your lifetime earnings, specifically your 35 highest-earning years. The SSA uses a complex formula to determine your Primary Insurance Amount (PIA), which is the monthly benefit you would receive if you start collecting at your Full Retirement Age (FRA).

Average Indexed Monthly Earnings (AIME)

The first step in calculating your PIA involves determining your Average Indexed Monthly Earnings (AIME). This process adjusts your past earnings to account for changes in average wages over time. This indexing ensures that your past earnings are expressed in terms of their current value, providing a more accurate reflection of your lifetime contributions to Social Security. For example, earnings from 30 years ago are adjusted upwards to reflect today’s wage levels. The highest 35 years of these indexed earnings are then summed and divided by 420 (the number of months in 35 years) to arrive at your AIME.

Bend Points and the PIA Formula

Once your AIME is established, the SSA applies a progressive formula using ‘bend points’ to calculate your PIA. Bend points are specific dollar amounts that define the thresholds at which different percentages of your AIME are used. For instance, a certain percentage of your AIME up to the first bend point is included, a smaller percentage of your AIME between the first and second bend points is added, and an even smaller percentage of your AIME above the second bend point is included. This progressive structure means that lower-income earners receive a higher percentage of their average indexed earnings back in benefits compared to higher-income earners, reflecting the program’s social adequacy goals.

Cost-of-Living Adjustments (COLA)

After you begin receiving benefits, your payments are subject to annual Cost-of-Living Adjustments (COLA). COLA is designed to ensure that the purchasing power of Social Security benefits is not eroded by inflation. These adjustments are typically announced in October each year and take effect in December, impacting benefits paid starting in January of the following year. The COLA is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Understanding COLA is particularly important when discussing the 1.5% impact on 2026 Social Security Benefits, as it directly relates to maintaining the value of your income.

Factors Influencing 2026 Social Security Benefits

Several key factors converge to shape the future of 2026 Social Security Benefits. These include economic indicators, demographic trends, legislative decisions, and the health of the Social Security trust funds. Each plays a vital role in determining the benefit structure and the potential adjustments retirees can expect.

Economic Projections and Inflation

The state of the economy is a primary driver of Social Security adjustments. Inflation, as measured by the CPI-W, directly influences the COLA. If inflation remains moderate, as current projections suggest for the period leading up to 2026, the COLA might be lower than in periods of high inflation. The projected 1.5% impact on 2026 Social Security Benefits likely reflects a moderate inflationary environment, where the cost of living is rising but not dramatically. Wage growth also plays a role, as it affects the national average wage index, which in turn influences the indexing of past earnings and the bend points.

Demographic Shifts and the Worker-to-Beneficiary Ratio

Demographic trends, particularly the aging of the population and declining birth rates, pose long-term challenges to the Social Security system. As the baby boomer generation continues to enter retirement, the ratio of workers contributing to the system compared to beneficiaries receiving payments is shrinking. This imbalance can put pressure on the trust funds and may prompt discussions about future adjustments to benefits or payroll taxes. While the 1.5% impact for 2026 is an annual adjustment, the broader demographic picture informs the long-term sustainability and potential for more significant structural changes to 2026 Social Security Benefits and beyond.

Legislative and Policy Considerations

While the annual COLA is determined by a formula, Congress can enact legislation that affects Social Security benefits. Historically, legislative changes have included adjustments to the full retirement age, the taxation of benefits, or the benefit formula itself. While there are no immediate legislative changes specifically targeting a 1.5% adjustment for 2026, the ongoing debate about Social Security’s long-term solvency means that legislative action is always a possibility. Any significant policy changes could override or modify the standard calculations for 2026 Social Security Benefits, making it crucial for beneficiaries to stay updated on political discussions.

The Health of the Social Security Trust Funds

The Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI) trust funds are the financial bedrock of the Social Security program. The annual Trustees’ Report provides projections on the solvency of these funds. While they are currently able to pay full benefits, projections indicate that they may only be able to pay a certain percentage of scheduled benefits in the future if no legislative action is taken. The financial health of these trust funds indirectly influences the annual adjustments and the broader outlook for 2026 Social Security Benefits, as concerns about solvency can lead to calls for benefit modifications or revenue increases.

The Projected 1.5% Impact on 2026 Social Security Benefits

The specific projection of a 1.5% impact on 2026 Social Security Benefits is a crucial figure for current and future retirees. This percentage typically refers to the Cost-of-Living Adjustment (COLA) that beneficiaries might expect. While it’s still a projection and subject to change based on actual economic data, understanding its implications is vital for financial planning.

What Does a 1.5% COLA Mean for Your Benefits?

A 1.5% COLA means that, if this projection holds, your monthly Social Security benefit will increase by 1.5% starting in January 2026. For example, if you currently receive $1,500 per month, a 1.5% increase would add $22.50 to your monthly check, bringing it to $1,522.50. While this might seem like a modest increase, it’s designed to help your benefits keep pace with the rising cost of everyday goods and services. It’s important to remember that this adjustment is applied to your gross benefit amount before any deductions, such as Medicare Part B premiums.

How is the COLA Determined?

The COLA is determined by the increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the previous year to the third quarter of the current year. The SSA compares the average CPI-W for July, August, and September of the current year with the average for the same three months of the last year in which a COLA was effective. If there is an increase, the COLA is the percentage increase, rounded to the nearest one-tenth of one percent. The projection of 1.5% for 2026 Social Security Benefits is based on current economic forecasts for inflation in the coming years.

Comparing 1.5% to Historical COLAs

It’s useful to put the 1.5% projection into historical context. COLAs have varied significantly over the years, ranging from 0% in some years (when there was no measurable inflation) to much higher percentages during periods of high inflation. For example, in recent years, we’ve seen COLAs that were significantly higher due to elevated inflation, such as the 5.9% for 2022 and 8.7% for 2023. A 1.5% increase for 2026 Social Security Benefits would represent a return to a more moderate COLA environment, reflecting potentially lower inflationary pressures. This comparison helps retirees gauge the expected purchasing power of their benefits.

Navigating the New Calculations and Their Impact

Understanding the new calculations and the projected 1.5% impact on 2026 Social Security Benefits is just the first step. The next is to strategically navigate these changes to ensure your retirement plan remains robust. This involves proactive planning, considering various claiming strategies, and staying informed.

Re-evaluating Your Retirement Budget

With a projected 1.5% increase, it’s a good time to re-evaluate your retirement budget. While any increase is welcome, a modest COLA means that other expenses might be rising at a faster rate. Review your monthly expenditures, particularly those susceptible to inflation, such as healthcare, housing, and groceries. Adjust your budget to reflect the updated benefit amount and to identify any areas where you might need to make adjustments to maintain your desired lifestyle. This proactive budgeting is crucial for managing your 2026 Social Security Benefits effectively.

Considering Claiming Strategies

The timing of when you claim your Social Security benefits can significantly affect your lifetime income. While the 1.5% adjustment applies to whatever benefit amount you are eligible for, strategic claiming can maximize that base amount. For instance, delaying benefits beyond your Full Retirement Age (FRA) can result in an 8% increase per year up to age 70. Conversely, claiming early (as early as age 62) results in a permanent reduction. Use the SSA’s online tools and consider consulting a financial advisor to determine the optimal claiming strategy that aligns with your financial situation and longevity expectations, especially in light of the projected 2026 Social Security Benefits.

Impact on Medicare Premiums

It’s important to remember that Medicare Part B premiums are often deducted directly from Social Security benefits. While a 1.5% COLA will increase your gross benefit, an increase in Medicare premiums could offset some or all of that gain. The ‘hold harmless’ provision generally prevents your Part B premium from increasing if it would cause your net Social Security benefit to decrease. However, this provision doesn’t apply to everyone, particularly those new to Medicare or those with higher incomes subject to Income-Related Monthly Adjustment Amounts (IRMAA). Factor potential Medicare premium increases into your overall financial planning for 2026 Social Security Benefits.

The Future of Social Security: Long-Term Outlook

While we focus on the immediate impact of 2026 Social Security Benefits, it’s also prudent to consider the program’s long-term outlook. The Social Security Trustees project that the trust funds will be able to pay 100% of scheduled benefits until the mid-2030s, after which they may only be able to pay about 80% of scheduled benefits if Congress does not act. This long-term solvency challenge underscores the importance of not relying solely on Social Security for retirement and diversifying your retirement income sources. Staying informed about legislative proposals and advocating for solutions can also play a role in securing the future of the program.

Strategies for Maximizing Your Retirement Income

Given the projected 1.5% impact on 2026 Social Security Benefits, and the broader context of retirement finances, it’s more important than ever to adopt strategies that maximize your overall retirement income. Social Security is a vital component, but it should ideally be part of a multi-faceted approach.

Diversifying Retirement Savings

Relying solely on Social Security for retirement is a risky proposition for most individuals. To build a resilient retirement income stream, diversification is key. This includes contributing regularly to other tax-advantaged accounts such as 401(k)s, IRAs (Traditional or Roth), and potentially other investment vehicles. A diversified portfolio can provide a buffer against economic fluctuations and ensure you have multiple income sources to draw upon, complementing your 2026 Social Security Benefits.

Working Longer or Part-Time

For many, working a few extra years can significantly impact retirement finances. Delaying retirement allows for additional savings, potentially higher Social Security benefits (due to delayed claiming credits and more high-earning years), and a shorter retirement period over which savings need to last. Even working part-time in retirement can provide supplemental income, cover unexpected expenses, and reduce the strain on your savings and 2026 Social Security Benefits.

Optimizing Investment Strategies

As you approach and enter retirement, your investment strategy should shift from growth-oriented to income-oriented, while still maintaining some exposure to growth to combat inflation. Consider investments that generate income, such as dividends stocks, bonds, or real estate, to supplement your Social Security checks. Regularly review your portfolio with a financial advisor to ensure it aligns with your risk tolerance and income needs, especially as you factor in the adjustments to 2026 Social Security Benefits.

Understanding Taxation of Benefits

Depending on your combined income, a portion of your Social Security benefits may be taxable at the federal level, and in some states. Understanding these thresholds and planning for potential taxes on your 2026 Social Security Benefits can help you avoid surprises and manage your cash flow more effectively. For instance, if your combined income (adjusted gross income + non-taxable interest + one-half of your Social Security benefits) exceeds certain limits, up to 85% of your benefits could be subject to federal income tax.

Preparing for Future Social Security Changes

The projected 1.5% impact on 2026 Social Security Benefits is a reminder that the program is dynamic. Future changes, whether related to COLA, eligibility, or taxation, are inevitable. Proactive preparation is the best defense against unforeseen financial challenges.

Regularly Reviewing Your Social Security Statement

The Social Security Administration provides annual statements detailing your earnings history and estimated future benefits. Regularly reviewing your statement is crucial to ensure your earnings record is accurate and to get a clear picture of your projected benefits. Any errors in your earnings history could negatively impact your future 2026 Social Security Benefits and beyond. You can access your statement online by creating an account at my Social Security.

Staying Informed About Legislation

As mentioned earlier, legislative action can significantly alter Social Security. Stay informed about proposals and debates concerning the program’s solvency and structure. Reputable financial news outlets, government websites, and advocacy groups are excellent resources for tracking potential changes that could affect your 2026 Social Security Benefits and your overall retirement plan.

Consulting with a Financial Advisor

A qualified financial advisor can provide personalized guidance tailored to your specific situation. They can help you understand how potential changes to 2026 Social Security Benefits might affect your overall financial plan, explore claiming strategies, optimize your investment portfolio, and develop a comprehensive retirement income strategy that accounts for various contingencies. Their expertise can be invaluable in navigating complex financial decisions.

Building an Emergency Fund

An emergency fund is a cornerstone of any sound financial plan, but it becomes even more critical in retirement. Unexpected expenses, healthcare costs, or periods of lower-than-expected Social Security adjustments can be mitigated with a robust emergency fund. Aim for at least six to twelve months’ worth of living expenses in an easily accessible, liquid account. This financial safety net provides peace of mind and reduces reliance on your fixed 2026 Social Security Benefits for unexpected costs.

Conclusion: Securing Your Retirement with 2026 Social Security Benefits in Mind

The discussion around 2026 Social Security Benefits, particularly the projected 1.5% impact, highlights the continuous need for vigilance and proactive planning in retirement. While Social Security provides a foundational income stream, it is crucial to view it as one component of a broader, diversified financial strategy.

Understanding the intricacies of benefit calculations, the factors that influence annual adjustments like COLA, and the long-term outlook for the program empowers you to make informed decisions. The 1.5% adjustment for 2026, while seemingly small, underscores the importance of budgeting carefully, considering optimal claiming strategies, and diversifying your retirement savings to account for both anticipated and unanticipated changes.

As you plan for 2026 and beyond, remember to regularly review your Social Security statement, stay abreast of legislative developments, and consult with financial professionals. By taking these steps, you can ensure that your retirement income, including your 2026 Social Security Benefits, remains resilient and continues to support the retirement lifestyle you envision.

Ultimately, securing your financial well-being in retirement requires a holistic approach. Social Security is a powerful tool, but its effectiveness is maximized when integrated into a comprehensive plan that includes personal savings, investments, and thoughtful management of expenses. Embrace the opportunity to review and refine your strategy now, ensuring you are well-prepared for the financial landscape of 2026 and the many years of retirement ahead.