2026 Student Loan Forgiveness: Eligibility, Programs & Application Deadlines

The landscape of student loan debt in the United States is a dynamic and often challenging one. With millions of Americans shouldering significant educational debt, the prospect of student loan forgiveness offers a beacon of hope. As we approach 2026, many borrowers are eagerly looking for clarity on available programs, eligibility requirements, and crucial application deadlines. This comprehensive guide aims to demystify the process, providing U.S. borrowers with the essential information needed to navigate the complexities of student loan forgiveness in 2026.

Understanding the nuances of federal and state-specific programs, along with potential new initiatives, is paramount. The information presented here is designed to be a definitive resource, helping you identify opportunities to reduce your financial burden and achieve greater financial stability. Let’s delve into the specifics of student loan forgiveness 2026.

Student loan debt has become a pervasive issue, impacting individuals from all walks of life. The sheer volume of outstanding debt can feel overwhelming, but various programs exist to alleviate this burden. Forgiveness, discharge, and cancellation are terms often used interchangeably, but they can have distinct meanings depending on the program. Generally, ‘forgiveness’ refers to the cancellation of a portion or all of your student loan debt, meaning you are no longer required to repay it. This can happen under specific circumstances, such as working in public service, experiencing a permanent disability, or if your school closes.

The federal government, through the Department of Education, is the primary administrator of most student loan forgiveness programs. However, state governments and even some private organizations offer their own initiatives. It’s crucial for borrowers to understand which type of loans they hold (federal vs. private) as most forgiveness options apply exclusively to federal student loans. Private student loans rarely offer forgiveness, though they may have options for deferment or forbearance in times of financial hardship.

As we plan for 2026, it’s important to remember that policies can evolve. While this guide provides the most current and anticipated information, staying updated with official government announcements is always recommended. The goal is to empower you with knowledge, enabling you to make informed decisions about your financial future and take advantage of any opportunities for student loan forgiveness 2026.

The Current Landscape of Student Loan Forgiveness Programs

Before diving into future possibilities, it’s essential to understand the existing federal student loan forgiveness programs that are expected to continue into 2026. These programs have specific criteria, and meeting them is key to successful debt relief.

Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness (PSLF) program is arguably one of the most well-known and impactful federal initiatives. It offers tax-free forgiveness of the remaining balance on Direct Loans after borrowers have made 120 qualifying monthly payments while working full-time for a qualifying employer. Qualifying employers include government organizations (federal, state, local, or tribal), non-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code, and other non-profit organizations that provide certain public services.

Eligibility for PSLF:

- Loan Type: Only Direct Loans qualify. If you have Federal Family Education Loan (FFEL) Program loans or Federal Perkins Loans, you’ll need to consolidate them into a Direct Consolidation Loan to be eligible.

- Employment: You must work full-time for a qualifying public service employer. Full-time generally means working at least 30 hours per week or whatever your employer considers full-time, whichever is greater.

- Payments: You must make 120 qualifying monthly payments. These payments must be made under a qualifying income-driven repayment (IDR) plan, on time, for the full amount due, and while employed full-time by a qualifying employer.

It’s critical for PSLF applicants to certify their employment annually or whenever they change employers using the PSLF Help Tool on the Federal Student Aid website. This helps track progress and avoid issues later. Borrowers aiming for student loan forgiveness 2026 through PSLF should start this process immediately if they haven’t already.

Income-Driven Repayment (IDR) Plan Forgiveness

Income-Driven Repayment (IDR) plans are designed to make federal student loan payments more manageable by capping them at a percentage of your discretionary income. A significant benefit of these plans is that any remaining loan balance is forgiven after 20 or 25 years of payments, depending on the specific IDR plan and whether you have loans for graduate study.

Types of IDR Plans:

- Revised Pay As You Earn (REPAYE) Plan: Generally 10% of discretionary income. Forgiveness after 20 years for undergraduate loans, 25 years for graduate loans.

- Pay As You Earn (PAYE) Plan: Generally 10% of discretionary income. Forgiveness after 20 years.

- Income-Based Repayment (IBR) Plan: Generally 10% or 15% of discretionary income, depending on when you took out your loans. Forgiveness after 20 or 25 years.

- Income-Contingent Repayment (ICR) Plan: The lesser of 20% of discretionary income or what you would pay on a fixed 12-year payment plan, adjusted for income. Forgiveness after 25 years.

It’s important to note that unlike PSLF, the forgiven amount under IDR plans may be considered taxable income by the IRS, unless Congress extends the provision that makes it tax-free, which is currently set to expire in 2025. This is a crucial consideration for anyone planning for student loan forgiveness 2026 via IDR plans.

Teacher Loan Forgiveness

This program is specifically for teachers who work in low-income schools or educational service agencies. Eligible teachers can have up to $17,500 of their Direct Subsidized and Unsubsidized Loans and their Subsidized and Unsubsidized Federal Stafford Loans forgiven. To qualify, you must teach full-time for five complete and consecutive academic years in a low-income school or educational service agency.

Key Requirements:

- Loan Type: Direct Subsidized/Unsubsidized Loans and Federal Stafford Loans.

- Teaching Service: Five consecutive full-time years of teaching in a qualifying low-income school.

- Certification: Your school or agency must be listed in the Annual Directory of Designated Low-Income Schools for Teacher Cancellation Benefits.

The amount of forgiveness depends on your subject area. Highly qualified math, science, or special education teachers can receive up to $17,500, while other qualified teachers can receive up to $5,000.

Total and Permanent Disability (TPD) Discharge

Borrowers who are totally and permanently disabled may be eligible for a Total and Permanent Disability (TPD) discharge, which relieves them from repaying their federal student loans. This discharge can be granted through three methods: documentation from the Department of Veterans Affairs (VA), documentation from the Social Security Administration (SSA), or certification from a physician.

Eligibility for TPD Discharge:

- VA Documentation: If the VA determines you have a service-connected disability that is 100% disabling or you are unemployable due to a service-connected condition.

- SSA Documentation: If you are receiving Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) benefits and your next scheduled disability review is 5-7 years or more from your most recent disability determination.

- Physician’s Certification: A licensed medical doctor must certify that you are unable to engage in any substantial gainful activity due to a physical or mental impairment that can be expected to result in death, has lasted for a continuous period of at least 60 months, or can be expected to last for a continuous period of at least 60 months.

It’s important to note that there is a post-discharge monitoring period (typically three years) during which certain conditions must be met to maintain the discharge. Income above the poverty line and new student loan borrowing can revoke the discharge. This program provides significant relief for eligible individuals seeking student loan forgiveness 2026.

Borrower Defense to Repayment

This program provides relief to students who were misled by their colleges. If your school engaged in misconduct, such as making false promises about job prospects or transferring credits, you might be eligible to have your federal student loans discharged. This is typically applicable when a school closes or if the borrower can prove the school defrauded them.

Key Considerations:

- Proof of Misconduct: You must demonstrate that your school violated certain state laws related to educational services or made specific misrepresentations.

- Federal Loans Only: This applies exclusively to federal student loans.

- Application Process: Requires submitting an application with supporting documentation to the Department of Education.

The process for borrower defense has seen significant changes over the years, with varying levels of relief offered. Borrowers should stay informed about the latest policies if they believe they have a claim.

Anticipated Changes and New Initiatives for 2026

While the existing programs form the backbone of student loan forgiveness, the political and economic climate often leads to discussions and potential implementation of new policies. As we look towards student loan forgiveness 2026, several areas could see significant developments.

Potential for Broad-Based Forgiveness

The discussion around broad-based student loan forgiveness has been a prominent topic in recent years. While significant universal forgiveness has not yet materialized, the conversation continues, and future administrations or legislative actions could introduce such measures. Borrowers should monitor political developments and official announcements from the Department of Education closely. Any broad forgiveness initiative would likely come with specific income caps and loan type restrictions.

Simplification of Existing Programs

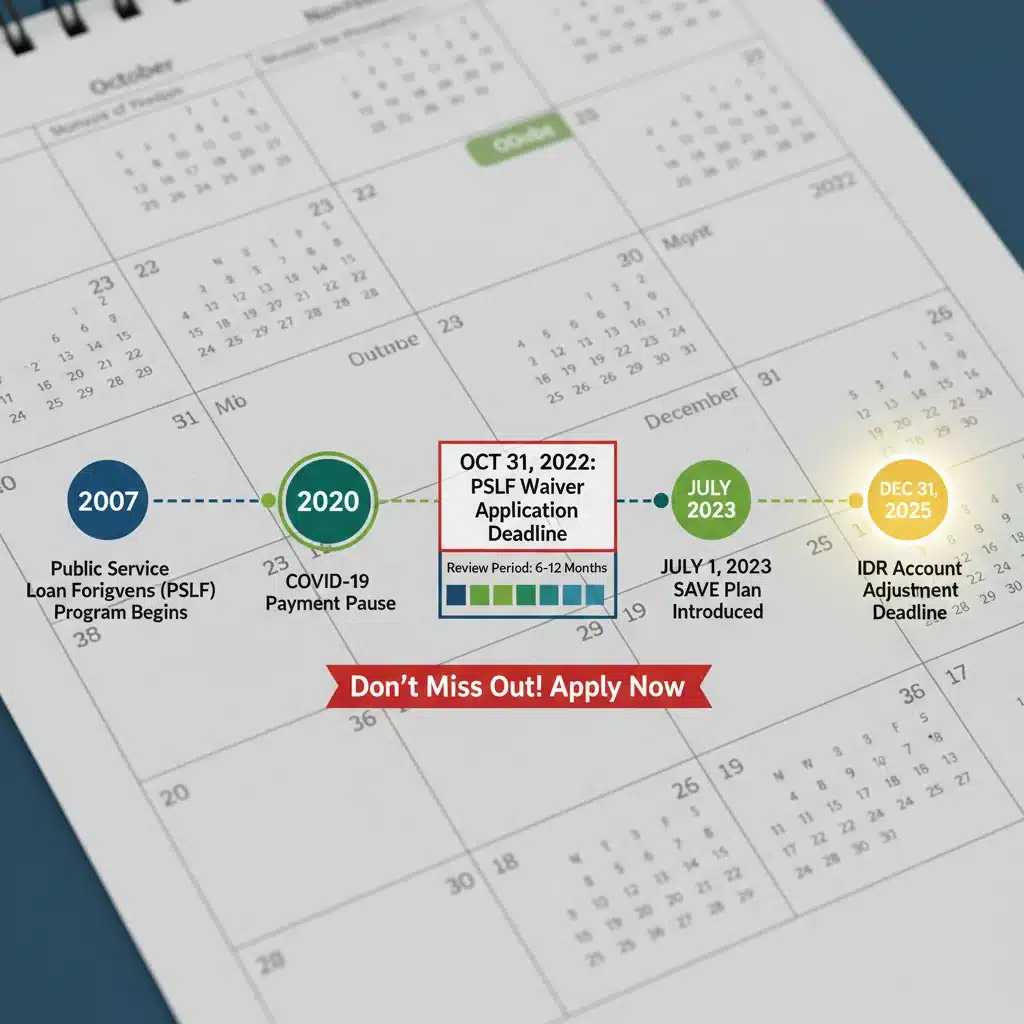

There is ongoing effort to simplify and streamline existing forgiveness programs, particularly PSLF and IDR plans. The Department of Education has made strides in this direction, such as the PSLF Waiver and IDR Account Adjustment, which allowed past payments that previously didn’t count to be credited towards forgiveness. These temporary measures have provided relief to many, and there’s a possibility of permanent reforms to make these programs more accessible and easier to navigate for future borrowers, impacting student loan forgiveness 2026.

State-Specific Loan Forgiveness Programs

Beyond federal initiatives, many states offer their own loan forgiveness or repayment assistance programs, often targeting specific professions in high-need areas. These can include programs for healthcare professionals (doctors, nurses), lawyers, teachers, and other public servants who commit to working in underserved communities for a certain period. Eligibility and benefits vary widely by state, so it’s crucial to research programs specific to your state of residence and profession.

For instance, some states offer loan repayment assistance for medical professionals who practice in rural or low-income areas, while others might help teachers working in critical shortage subjects or schools. These programs often complement federal aid and can significantly reduce your overall debt burden.

Eligibility Criteria: Are You on Track for Forgiveness in 2026?

Understanding the general eligibility criteria is the first step toward securing student loan forgiveness 2026. While specific program requirements vary, several common factors determine your eligibility.

Federal vs. Private Loans

The most critical distinction is between federal and private student loans. Almost all significant forgiveness programs apply only to federal student loans. Private loans, issued by banks or other financial institutions, typically do not offer forgiveness options, though lenders may provide deferment or forbearance in hardship cases. If you have private loans, your best recourse for relief might be refinancing to a lower interest rate, if your credit score allows, or exploring options with your lender.

Loan Types and Consolidation

Even among federal loans, certain types are more eligible than others. Direct Loans (Subsidized, Unsubsidized, PLUS) are generally the most versatile for forgiveness programs. Older loan types, such as Federal Family Education Loan (FFEL) Program loans or Federal Perkins Loans, often require consolidation into a Direct Consolidation Loan to become eligible for PSLF or IDR forgiveness. Consolidating your loans can simplify your payments and open up forgiveness pathways, but it’s essential to understand that consolidation can sometimes extend your repayment period or capitalize interest.

Employment Requirements

Many forgiveness programs, especially PSLF and Teacher Loan Forgiveness, have strict employment requirements. You must be employed full-time by a qualifying employer for a specified period. It’s not just about the type of job, but also the type of organization. Public service employers are often defined as government entities or 501(c)(3) non-profits. Verify your employer’s eligibility through official channels, such as the PSLF Help Tool.

Payment History

For programs like PSLF and IDR forgiveness, your payment history is paramount. You must make a certain number of qualifying payments. These payments typically need to be: on time, for the full amount due, made while employed by a qualifying employer (for PSLF), and under a qualifying repayment plan (usually an IDR plan for PSLF, or any plan for IDR forgiveness if you meet the payment count). Any periods of deferment, forbearance, or late payments might not count towards your forgiveness total, though recent adjustments have provided some flexibility.

Income and Family Size

For IDR plans, your income and family size are crucial factors. Your monthly payment is calculated based on a percentage of your discretionary income, which is the difference between your adjusted gross income (AGI) and a multiple of the poverty guideline for your family size. As your income or family size changes, your payments will be adjusted, and you must recertify your income and family size annually to remain on an IDR plan and continue making progress towards forgiveness.

Navigating the Application Process and Deadlines

The application process for student loan forgiveness can be complex and requires careful attention to detail. Missing deadlines or submitting incomplete information can delay or even jeopardize your chances of receiving student loan forgiveness 2026.

Staying Informed: Official Sources

The most reliable sources of information are the U.S. Department of Education’s Federal Student Aid (FSA) website (studentaid.gov) and your loan servicer. Be wary of third-party companies promising guaranteed forgiveness for a fee; many of these are scams. All federal student loan services are free. Regularly check the FSA website for updates on programs, policy changes, and deadlines.

Key Steps for Application:

- Identify Eligible Loans: Confirm whether your loans are federal and if they are eligible for the programs you are interested in. If necessary, consider consolidation.

- Choose the Right Program: Based on your employment, income, and loan types, determine which forgiveness program aligns best with your situation.

- Enroll in a Qualifying Repayment Plan: For PSLF and IDR forgiveness, ensure you are on an eligible income-driven repayment plan.

- Track Your Progress: For PSLF, use the PSLF Help Tool to certify your employment annually and ensure your payments are being counted. Keep meticulous records of all your payments and employment history.

- Submit the Application: Once you meet the requirements (e.g., 120 qualifying payments for PSLF, or 20/25 years for IDR), submit the appropriate application form to your loan servicer.

- Respond to Requests: Be prepared to respond promptly to any requests for additional documentation or information from your loan servicer or the Department of Education.

Important Deadlines for 2026 and Beyond

While many forgiveness programs are ongoing, there can be specific deadlines for certain actions or temporary initiatives. For instance, the PSLF Waiver had a deadline, but its impact continues to be processed. Similarly, the IDR Account Adjustment is also being implemented. Borrowers should regularly check their loan servicer’s website and studentaid.gov for any upcoming deadlines related to these or potential new programs.

For IDR plans, the most critical annual deadline is the recertification of your income and family size. Failing to recertify on time can lead to your payments increasing and capitalized interest. Mark your calendar for this annual requirement. For PSLF, while there isn’t a hard deadline to apply, certifying your employment annually is highly recommended to ensure your payments are being tracked correctly and to prevent any surprises when you eventually apply for forgiveness.

Common Pitfalls and How to Avoid Them

The path to student loan forgiveness is not always straightforward. Many borrowers encounter obstacles that can delay or prevent them from receiving the relief they deserve. Being aware of these common pitfalls can help you navigate the process more effectively for student loan forgiveness 2026.

Incorrect Loan Types

One of the most frequent issues is having the wrong type of federal loan. As mentioned, FFEL and Perkins Loans often need to be consolidated into Direct Loans to qualify for PSLF or IDR forgiveness. Many borrowers are unaware of this requirement until it’s too late. Always confirm your loan type and take the necessary steps to consolidate if needed, understanding the implications of consolidation.

Non-Qualifying Employment or Payments for PSLF

For PSLF, defining ‘qualifying employment’ and ‘qualifying payments’ can be tricky. Working for a for-profit company, even if it provides public services, generally does not count. Similarly, payments made under non-IDR plans (like the Standard Repayment Plan for more than 10 years, or Graduated Repayment Plans) or payments made while not employed full-time by a qualifying employer do not count. Using the PSLF Help Tool and certifying employment regularly is crucial to avoid this pitfall.

Forgetting to Recertify IDR Plans

Annual recertification of income and family size for IDR plans is mandatory. If you fail to recertify, your monthly payment will likely increase, and any unpaid interest may be capitalized (added to your principal balance), increasing your overall debt. Set reminders and ensure you submit your documentation on time each year.

Falling Victim to Scams

Unfortunately, the student loan landscape is ripe for scams. Companies often advertise services that promise quick or guaranteed forgiveness for a fee. Remember: you never have to pay for federal student loan assistance. All services related to federal loans, including applying for forgiveness, are free through the Department of Education and your loan servicer. Be highly skeptical of unsolicited offers or requests for your FSA ID password.

Lack of Documentation

Keeping meticulous records is vital. This includes copies of all loan documents, payment confirmations, employment certification forms, and any correspondence with your loan servicer or the Department of Education. If there’s a discrepancy in your payment count or eligibility, having thorough documentation can be the key to resolving the issue.

Strategies for Maximizing Your Forgiveness Potential

To optimize your chances of receiving student loan forgiveness 2026, a proactive and informed approach is essential. Here are some strategies:

Regularly Check Your Loan Status

Log into your Federal Student Aid account (studentaid.gov) frequently. Review your loan types, current repayment plan, and payment history. Ensure all information is accurate and up-to-date. If you have multiple servicers, make sure to check all of them.

Communicate with Your Loan Servicer

Your loan servicer is your primary point of contact for managing your federal student loans. Don’t hesitate to reach out to them with questions about your eligibility, payment counts, or application status. Keep a record of all communications, including dates, names of representatives, and summaries of conversations.

Consider Loan Consolidation Carefully

While consolidation can open doors to certain forgiveness programs, it also has implications. It combines multiple federal loans into one, potentially extending your repayment term and capitalizing interest. Research thoroughly and speak with your servicer before consolidating, especially if you have older loans with lower interest rates or unique benefits.

Understand Tax Implications

As noted, IDR forgiveness may be subject to federal income tax, while PSLF is tax-free. This is a significant difference that can impact your financial planning. Consult with a tax professional to understand the potential tax burden of any forgiven amount, especially if the current tax-free status of IDR forgiveness is not extended beyond 2025.

Explore Employer Benefits

Some employers offer their own student loan repayment assistance programs as a benefit. These can be in addition to federal programs. Check with your HR department to see if your employer provides any such support, which could contribute to your overall student loan forgiveness 2026 strategy.

Advocate for Policy Changes

Stay informed about ongoing discussions regarding student loan policy and consider engaging with advocacy groups. Collective action and public discourse can influence future legislative decisions that may lead to broader or more accessible forgiveness programs.

Conclusion: Preparing for Student Loan Forgiveness in 2026

The journey to student loan forgiveness can be long and intricate, but with careful planning and consistent effort, it is an achievable goal for many U.S. borrowers. As we look towards student loan forgiveness in 2026, the key is to be proactive, informed, and diligent.

Begin by understanding the specific types of federal loans you hold and whether they qualify for existing forgiveness programs like PSLF or IDR. Take the necessary steps to consolidate if required, and ensure you are enrolled in the most appropriate repayment plan for your financial situation and forgiveness goals. Regularly certify your employment for PSLF and recertify your income for IDR plans to keep your progress on track.

Stay vigilant against scams and rely only on official government sources and your loan servicer for information. Keep meticulous records of all your interactions and payments. By avoiding common pitfalls and implementing smart strategies, you can significantly increase your chances of receiving substantial student loan relief.

Remember, the landscape of student loan policies is subject to change. Continuously monitor updates from the Department of Education and your loan servicer to adapt your strategy as needed. With dedication and the right information, student loan forgiveness 2026 can become a reality, paving the way for a more secure financial future.