Student Loan Forgiveness 2026: New Programs & Eligibility for 1.2 Million

The landscape of student loan debt in the United States is constantly evolving, and for millions of borrowers, the prospect of relief is a persistent hope. As we look ahead to 2026, significant changes and new benefit programs are being implemented that could profoundly impact approximately 1.2 million individuals seeking student loan forgiveness 2026. Understanding these developments is crucial for anyone navigating the complexities of their educational debt. This comprehensive guide will delve into the anticipated updates, eligibility requirements, and the broader implications of these new initiatives, providing clarity and actionable insights for borrowers across the nation.

For many, student loans represent a substantial financial burden, influencing major life decisions from career paths to homeownership. The federal government, recognizing the widespread impact of this debt, has continued to explore and implement strategies aimed at providing relief. The year 2026 is poised to bring forth a new wave of opportunities for student loan forgiveness, building upon previous efforts and introducing targeted programs designed to address specific borrower needs. These initiatives are not just about alleviating individual debt; they are also about stimulating economic growth and fostering greater educational accessibility.

The journey to student loan forgiveness 2026 can be intricate, with various programs, criteria, and application processes. It’s essential for borrowers to stay informed and proactive. This article aims to demystify these processes, offering a clear roadmap to understanding what these new programs entail, who stands to benefit, and what steps need to be taken to capitalize on these opportunities. We will explore the nuances of income-driven repayment plans, public service loan forgiveness, and other specialized programs, ensuring that you have a holistic view of your potential options.

Understanding the Current Student Loan Landscape

Before diving into the specifics of student loan forgiveness 2026, it’s important to grasp the current state of student debt. Millions of Americans collectively owe trillions of dollars in student loans, a figure that continues to grow. This debt is held by individuals from various backgrounds, including recent graduates, mid-career professionals, and even retirees. The economic implications are far-reaching, affecting consumer spending, entrepreneurship, and overall financial stability.

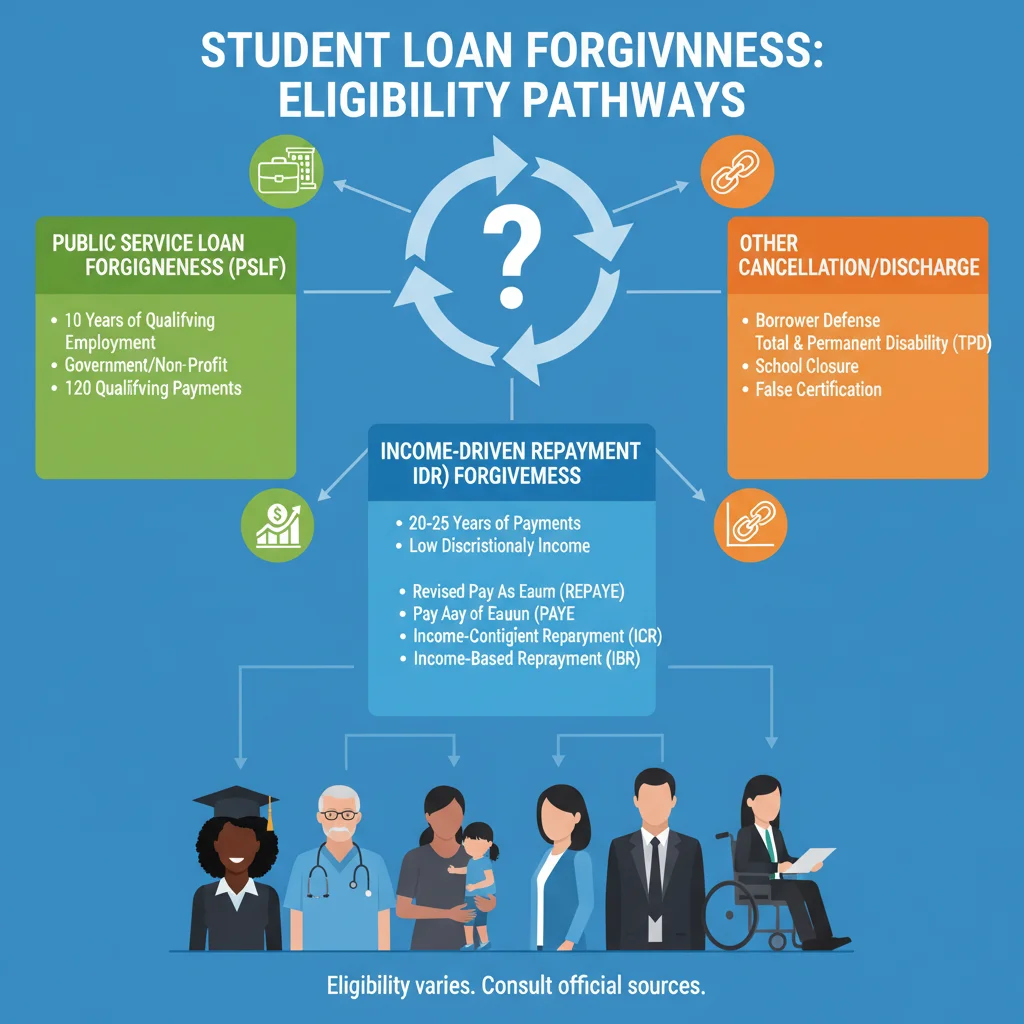

Historically, federal student loan programs have offered various repayment plans, including standard, graduated, extended, and income-driven repayment (IDR) plans. IDR plans, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR), have been particularly significant because they offer a path to forgiveness after a certain number of years of qualifying payments. However, these plans have often been criticized for their complexity and the challenges borrowers face in tracking their progress toward forgiveness.

The Public Service Loan Forgiveness (PSLF) program is another cornerstone of federal student loan relief, designed for borrowers who work in qualifying public service jobs. While PSLF has offered substantial relief to many, it has also faced its share of administrative hurdles and confusion, leading to low approval rates in its early years. Continuous efforts have been made to streamline PSLF and expand its reach, setting the stage for further enhancements in 2026.

The past few years have also seen significant policy shifts, including temporary payment pauses and targeted forgiveness initiatives. These measures have brought both relief and uncertainty, highlighting the dynamic nature of student loan policy. As we approach 2026, the focus is on creating more sustainable, equitable, and transparent pathways to debt relief, aiming to address the systemic issues that have contributed to the student loan crisis.

New Benefit Programs for Student Loan Forgiveness 2026

The year 2026 is anticipated to bring forth several new or significantly enhanced benefit programs under the umbrella of student loan forgiveness 2026. These programs are designed to be more accessible, equitable, and impactful, targeting specific groups of borrowers and addressing common pitfalls of previous initiatives. While exact details are still being finalized, general frameworks and objectives have been outlined.

Streamlined Income-Driven Repayment (IDR) Plans

One of the most significant changes expected is the continued evolution and simplification of income-driven repayment plans. The goal is to make these plans easier to understand, enroll in, and manage, ultimately leading to more borrowers successfully reaching forgiveness. This could involve:

- Lower Discretionary Income Calculation: A reduction in the percentage of discretionary income used to calculate monthly payments, making payments more affordable for a larger number of borrowers.

- Shorter Repayment Periods: Forgiveness timelines could be shortened for certain borrowers, particularly those with lower original loan balances. This aims to provide relief sooner, rather than requiring decades of payments.

- Automatic Enrollment and Recertification: Efforts to automate enrollment in IDR plans for eligible borrowers and simplify the annual income recertification process, reducing administrative burdens and preventing lapses in qualifying payments.

- Expanded Eligibility: Potentially broadening the definition of eligible income or household size to include more borrowers who are struggling financially.

These changes are critical as IDR plans are often the primary pathway to forgiveness for millions of borrowers who do not qualify for PSLF or other specialized programs. A more robust and user-friendly IDR system is central to the broader strategy for student loan forgiveness 2026.

Targeted Forgiveness for Specific Professions and Circumstances

Beyond general IDR improvements, 2026 may also see the introduction or expansion of targeted forgiveness programs for individuals in high-need professions or those facing unique circumstances. These could include:

- Healthcare Workers: Enhanced forgiveness options for nurses, doctors, and other medical professionals, especially those serving in underserved communities.

- Educators: Expanded programs for teachers, particularly those in low-income schools or teaching critical shortage subjects.

- Early Childhood Educators: Specific relief for professionals in the early childhood education sector, recognizing their vital role and often lower salaries.

- Borrowers with Disabilities: Streamlined and expanded total and permanent disability (TPD) discharge processes, making it easier for eligible individuals to receive forgiveness.

- Borrowers with Long-Standing Debt: Initiatives to provide relief for borrowers who have been in repayment for an extended period, regardless of their income or profession, acknowledging the psychological and financial toll of prolonged debt.

These targeted programs aim to not only provide financial relief but also to incentivize careers in critical sectors and support vulnerable populations, aligning with broader societal goals.

Public Service Loan Forgiveness (PSLF) Enhancements

While PSLF has seen significant reforms in recent years, further enhancements are expected to solidify its effectiveness and reach more public servants. These could include:

- Simplification of Employer Certification: Making it easier for borrowers and employers to certify qualifying employment, reducing administrative errors and delays.

- Expanded Definition of Public Service: Potentially broadening the types of organizations or roles that qualify for PSLF, recognizing a wider range of public service contributions.

- Improved Payment Tracking: Better systems for tracking qualifying payments, providing borrowers with clearer progress reports and reducing uncertainty about their eligibility.

The goal is to ensure that PSLF truly serves its intended purpose: to encourage and reward individuals who dedicate their careers to public service, free from the burden of student debt after 10 years of qualifying payments.

Eligibility Requirements for 1.2 Million Borrowers

The new and improved programs for student loan forgiveness 2026 are projected to benefit approximately 1.2 million borrowers. However, eligibility is not universal and will depend on a combination of factors related to loan type, repayment history, income, and profession. Understanding these criteria is the first step toward determining if you qualify for relief.

Qualifying Loan Types

Generally, federal student loans are the primary candidates for forgiveness programs. This includes Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans. Federal Family Education Loan (FFEL) Program loans and Perkins Loans may also become eligible if they are consolidated into a Direct Consolidation Loan. Private student loans, however, are typically not eligible for federal forgiveness programs.

Income and Family Size

For income-driven repayment plans, your adjusted gross income (AGI) and family size are crucial determinants of your monthly payment amount and, consequently, your path to forgiveness. Most IDR plans cap payments at a percentage of your discretionary income, which is the difference between your AGI and a certain percentage of the federal poverty line. As mentioned, new programs may adjust this calculation to be more favorable to borrowers.

Repayment History and Time in Repayment

The length of time you have been in repayment is a key factor for most forgiveness programs. For IDR plans, forgiveness typically occurs after 20 or 25 years of qualifying payments, though the new initiatives may shorten this for some borrowers. For PSLF, 120 qualifying monthly payments (10 years) are required while working full-time for a qualifying employer.

It’s important to note that qualifying payments often refer to payments made while enrolled in an eligible repayment plan. Payments made during deferment, forbearance, or grace periods usually do not count, though some recent temporary waivers have allowed certain periods to count toward forgiveness.

Employment Type for PSLF

For those pursuing PSLF, working for a qualifying employer is paramount. This generally includes government organizations (federal, state, local, or tribal), not-for-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code, and other not-for-profit organizations that provide certain public services. The definition of ‘full-time’ employment also plays a role, typically meaning 30 hours or more per week.

Other Specific Criteria

For targeted forgiveness programs, specific criteria will apply. For instance, teacher loan forgiveness requires teaching for five complete consecutive academic years in a low-income school. Healthcare professional programs might require service in specific geographical areas or types of facilities. Borrowers with disabilities will need to meet the criteria for total and permanent disability as defined by federal regulations.

It is crucial for borrowers to carefully review the specific requirements for each program they are interested in, as even minor details can impact eligibility. The Department of Education and federal student aid websites will be the authoritative sources for the most up-to-date information on student loan forgiveness 2026.

The Application Process and Key Dates

Navigating the application process for student loan forgiveness 2026 requires diligence and attention to detail. While the exact procedures for new programs will be released closer to 2026, general guidelines and preparatory steps can be taken now.

Consolidate Your Loans (If Necessary)

If you have FFEL Program loans or Perkins Loans, consolidating them into a Direct Consolidation Loan is often a prerequisite for eligibility for many federal forgiveness programs, including PSLF and most IDR plans. This process combines multiple federal loans into a single new loan with a single interest rate and servicer, making it easier to manage and qualify for benefits.

Enroll in an Income-Driven Repayment Plan

For most paths to forgiveness, especially those not tied to public service, enrollment in an IDR plan is essential. You can apply for or change your repayment plan through your loan servicer or via the Federal Student Aid (FSA) website. Ensure you recertify your income and family size annually to keep your payments affordable and to continue counting toward forgiveness.

Track Your Payments and Employment

Maintaining meticulous records of your payments and, if applicable, your employment history is vital. For PSLF, use the PSLF Help Tool on the FSA website to certify your employment annually or whenever you change jobs. This tool helps ensure your employer qualifies and that your payments are being counted correctly. For IDR plans, keep records of your annual recertifications and any communication with your loan servicer.

Stay Informed About Program Updates

The landscape of student loan policy is dynamic. Regularly check the official Federal Student Aid website, subscribe to updates from the Department of Education, and consult reputable financial aid resources. This will ensure you are aware of any new programs, changes in eligibility, or application deadlines related to student loan forgiveness 2026.

Key Dates to Watch For

While specific dates for 2026 programs are not yet available, here are general types of dates to monitor:

- Program Announcements: Official announcements from the Department of Education about new forgiveness initiatives.

- Application Opening Dates: When applications for new programs become available.

- Recertification Deadlines: Annual deadlines for income-driven repayment plans.

- Waiver End Dates: If any temporary waivers are in effect, be aware of their expiration.

Proactive engagement with your loan servicer and the FSA website will be your best strategy for ensuring you don’t miss out on potential relief opportunities. Don’t wait until the last minute; begin preparing now.

Impact and Future Outlook of Student Loan Forgiveness 2026

The potential impact of student loan forgiveness 2026 on 1.2 million borrowers and the wider economy cannot be overstated. For individuals, debt relief can translate into increased financial flexibility, allowing them to pursue homeownership, start businesses, save for retirement, or invest in their communities. It can alleviate significant psychological stress, improving overall well-being and contributing to a healthier society.

Economically, reducing student loan burdens can stimulate consumer spending, as borrowers have more disposable income. This can boost various sectors, from retail to real estate. It can also encourage entrepreneurship, as individuals with less debt may feel more confident taking career risks. Furthermore, by addressing the student debt crisis, these programs contribute to greater economic equity, particularly for marginalized communities disproportionately affected by student loan burdens.

Challenges and Criticisms

Despite the positive intentions, student loan forgiveness programs often face challenges and criticisms. Concerns about fairness to those who have already paid off their loans, the potential for moral hazard (encouraging future borrowing without full consideration of repayment), and the overall cost to taxpayers are frequently raised. Policymakers must balance the need for relief with these broader economic and ethical considerations.

Another challenge is ensuring that the programs are effectively implemented and communicated. Past programs have sometimes suffered from administrative complexities, leading to confusion and frustration among borrowers. The success of the 2026 initiatives will depend heavily on clear guidance, efficient application processes, and robust support for borrowers.

Long-Term Solutions

While forgiveness programs offer crucial relief, they are often seen as a bandage rather than a cure for the underlying issues of higher education affordability. Long-term solutions will likely involve a multifaceted approach, including:

- Controlling Tuition Costs: Addressing the rising cost of higher education through policy changes, increased state funding for public institutions, and greater accountability for universities.

- Improved Financial Literacy: Educating students and families about the true cost of college, responsible borrowing, and available repayment options.

- Reforming the Federal Student Aid System: Continuously evaluating and improving the federal student aid programs to ensure they are effective, equitable, and sustainable.

- Investing in Workforce Development: Providing alternative pathways to high-paying careers that do not require a traditional four-year degree, reducing the pressure to incur significant student debt.

The student loan forgiveness 2026 initiatives represent a significant step in the ongoing effort to address student debt. However, they are part of a larger, evolving conversation about the future of higher education financing in the United States.

How to Prepare for Student Loan Forgiveness 2026

Even though 2026 is still some time away, proactive preparation is key to maximizing your chances of benefiting from upcoming student loan forgiveness programs. Here’s a checklist of actions you can take now:

- Review Your Loan Portfolio: Understand exactly what types of loans you have (federal vs. private), their current balances, interest rates, and servicers. This information is crucial for determining eligibility.

- Update Your Contact Information: Ensure your loan servicer and the Federal Student Aid (FSA) website have your most current mailing address, email, and phone number. This ensures you receive important updates and communications.

- Log In to Your FSA Account: Regularly check your account on StudentAid.gov. This portal is your primary resource for federal student loan information, including loan details, repayment history, and PSLF progress.

- Explore Income-Driven Repayment (IDR) Plans: If you are not already on an IDR plan, consider enrolling. Even if you don’t qualify for immediate forgiveness, being on an IDR plan is often a prerequisite for future forgiveness and ensures your payments are manageable.

- Certify Public Service Employment (If Applicable): If you work in public service, use the PSLF Help Tool to certify your employment annually. This helps ensure your payments are counted accurately and prevents issues down the line.

- Keep Detailed Records: Maintain a file (digital or physical) of all correspondence with your loan servicer, payment confirmations, employment certifications, and any other relevant documents. This can be invaluable if discrepancies arise.

- Seek Professional Advice: If your situation is complex, consider consulting with a non-profit credit counselor or a student loan expert. They can provide personalized guidance and help you navigate the various options.

- Stay Informed: Continue monitoring official sources for announcements regarding student loan forgiveness 2026. Policy changes can happen rapidly, and staying current is essential.

By taking these steps, you position yourself to take full advantage of any new or enhanced student loan forgiveness programs that become available in 2026. Don’t wait for announcements; start organizing your student loan information today.

Conclusion

The anticipation surrounding student loan forgiveness 2026 offers a glimmer of hope for 1.2 million borrowers grappling with educational debt. The expected rollout of new benefit programs, including streamlined income-driven repayment plans and targeted forgiveness initiatives, represents a significant commitment to alleviating the financial burden on individuals and stimulating broader economic growth. While the specifics are still unfolding, the overarching goal is to create more accessible, equitable, and effective pathways to debt relief.

For borrowers, the key to unlocking these opportunities lies in proactive engagement and informed decision-making. Understanding your loan types, tracking your repayment history, certifying your employment (if applicable), and staying vigilant about official announcements are crucial steps. The journey to student loan forgiveness can be complex, but with the right preparation and knowledge, you can navigate the process effectively and potentially secure the relief you deserve.

Ultimately, while these forgiveness programs are vital for immediate relief, they are also part of a larger dialogue about the future of higher education funding and accessibility. As we move towards 2026 and beyond, it is hoped that these initiatives, coupled with broader reforms, will not only address the current student debt crisis but also build a more sustainable and equitable educational system for generations to come. Stay informed, stay prepared, and take control of your financial future.